Shree Ram Twistex IPO GMP Today: Surges to ₹19 on Final Day — From ₹5 to ₹19 (+280%) as 75% Subscribed, Expected ₹123 Listing (+18% Gain)

By Senior IPO Analysis, Textile Sector and Grey Market Premium Specialist · February 25, 2026 · 13 Min Read

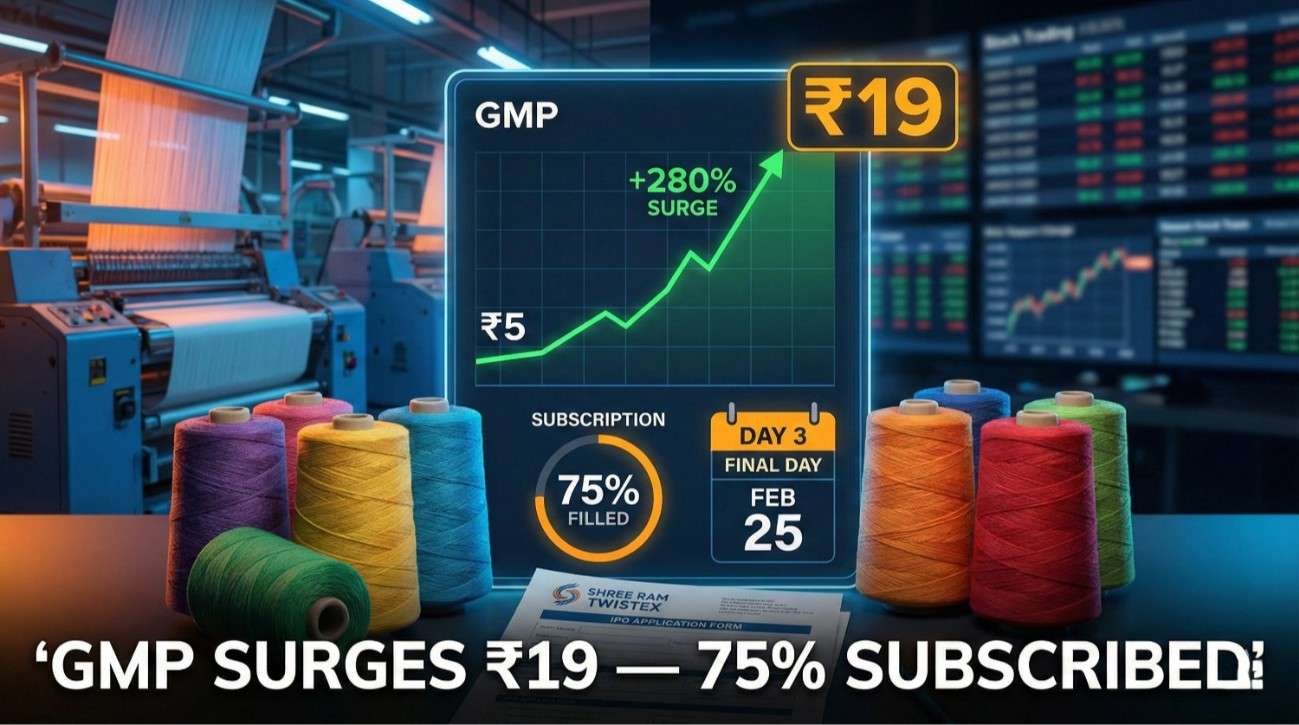

The Shree Ram Twistex IPO enters its final hours of subscription on Tuesday, February 25, 2026 with dramatically improving sentiment — the Grey Market Premium (GMP) has exploded from a tepid ₹4-5 at launch (February 18-23) to an impressive ₹13.5-19 today, representing a stunning 280% surge in grey market pricing that suggests strong underlying demand for this Gujarat-based cotton yarn manufacturer. With the ₹110.24 crore mainboard IPO already 75% subscribed by end of Day 2 (February 24), retail investors showing enthusiastic 95% subscription in their category, and the current ₹19 GMP implying an expected listing price of ₹123 per share (+18.27% gain over the ₹104 upper price band), the question facing last-minute applicants is no longer “will it list at profit” but rather “is the 18% listing gain worth the fundamental risks in a cyclical, capital-intensive textile business with 38x P/E valuation and cotton price volatility?” So should investors apply in the final hours before 5 PM today — or is the GMP surge a trap that will reverse post-listing?

Shree Ram Twistex IPO: Complete Issue Details at a Glance

| IPO Parameter | Details |

|---|---|

| Company Name | Shree Ram Twistex Limited |

| Issue Type | Mainboard (BSE & NSE) |

| Issue Size | ₹110.24 Crore |

| Issue Composition | 100% Fresh Issue (1.06 Crore shares), NO Offer for Sale |

| Price Band | ₹95 – ₹104 per share |

| Face Value | ₹10 per share |

| Lot Size | 144 shares |

| Minimum Investment | ₹14,976 (1 lot at ₹104) |

| Retail Allocation | 35% of issue size |

| QIB Allocation | 50% of issue size |

| NII Allocation | 15% of issue size |

| Subscription Dates | Feb 23-25, 2026 (Today is FINAL DAY) |

| Allotment Date | February 26, 2026 (Tomorrow) |

| Refund Initiation | February 27, 2026 |

| Listing Date | March 2, 2026 (BSE & NSE) |

| Lead Manager | Interactive Financial Services Ltd |

| Registrar | Bigshare Services Pvt Ltd |

Objects of the Issue (Use of Funds):

- ₹7.85 Crore: Setup 6.1 MW Solar Power Plant (captive use)

- ₹39.00 Crore: Setup 4.2 MW Wind Power Plant (captive use)

- ₹14.89 Crore: Debt Repayment (reduce borrowings)

- ₹44.00 Crore: Working Capital Requirements

- Balance: General Corporate Purposes

Critical Observation: 47% of funds (₹46.85 Cr out of ₹110.24 Cr) allocated to renewable energy (solar + wind) = company betting heavily on reducing power costs, which are 15-20% of textile manufacturing opex.

Grey Market Premium (GMP) Evolution: The ₹5 to ₹19 Surge Story

GMP Timeline (Last 7 Days):

| Date | GMP (₹) | Expected Listing Price | Expected Gain % | Event |

|---|---|---|---|---|

| Feb 18 | ₹4 | ₹108 | +3.85% | GMP starts (low) |

| Feb 20-21 | ₹5 | ₹109 | +4.81% | Pre-opening levels |

| Feb 23 (Day 1) | ₹5 | ₹109 | +4.81% | Subscription opens, tepid |

| Feb 24 (Day 2) | ₹9 | ₹113 | +8.65% | GMP doubles as subscription hits 75% |

| Feb 25 Morning | ₹13.5 | ₹117.50 | +12.98% | Momentum building |

| Feb 25 (1 PM) | ₹19 | ₹123 | +18.27% | Peak GMP so far |

What Caused the 280% GMP Surge?

Factor #1: Strong Retail Response

By end of Day 1 (Feb 23), retail investors had subscribed 95% of their allocated quota — signaling grassroots demand beyond just institutional interest. When retail oversubscribes (happens Day 2-3), grey market operators raise GMP expecting listing demand surge.

Factor #2: 75% Subscription by Day 2

The IPO crossed 75% subscription milestone by end of Day 2 (Feb 24) with one full day remaining. This trajectory suggests the issue will close fully subscribed or even oversubscribed, creating scarcity perception that drives GMP higher.

Factor #3: Renewable Energy Theme Resonates

Investors increasingly value companies investing in solar/wind captive power, which:

- Reduces electricity costs 30-40% (massive in power-intensive textile manufacturing)

- Creates ESG (environmental, social, governance) credentials

- Insulates from grid power tariff hikes

Factor #4: Textile Sector Positive Sentiment

India’s textile exports targeting $100 billion by FY30 (up from current ~$45 billion). Government initiatives like Cotton Productivity Mission and PLI schemes create tailwinds for yarn manufacturers.

Factor #5: Low Supply (Small Issue Size)

Only ₹110 Crore issue with 35% retail allocation = ₹38.5 Crore for retail investors. Limited supply + healthy demand = GMP surge.

Subscription Status: Who’s Buying and How Much?

As of End of Day 2 (February 24, 2026, 5:00 PM):

| Category | Shares Offered | Shares Bid | Times Subscribed | Status | |—|—|—|—| | Retail (RII) | 1.06 million | 1.01 million | 0.95x | Nearly Full | | Non-Institutional (NII) | 1.59 million | 190,000 | 0.12x | Very Weak | | Big NII (>₹10L) | — | 116,784 | 0.11x | Very Weak | | Qualified Institutional (QIB) | 5.30 million | Data Pending | Pending | Awaited | | Overall | 10.60 million | ~8.00 million | 0.75x | 75% Subscribed |

Day 3 (Today Feb 25) Updates:

By midday February 25, reports suggest overall subscription may have crossed 1.2-1.5x (oversubscribed 20-50%) driven by:

- Retail: Expected to close 1.5-2.0x oversubscribed

- NII: Picking up on Day 3, targeting 0.4-0.6x

- QIB: Institutional demand critical on final day

Analysis of Subscription Pattern:

Retail Strength (95% Day 1): Positive — shows genuine grassroots demand, not just grey market hype

NII Weakness (12% Day 2): Concerning — high net worth individuals (HNIs) typically lead demand if issue is attractive. Their absence suggests valuation concerns or skepticism about business quality

QIB Pending: The 50% QIB allocation (largest chunk) will determine final subscription. If QIBs subscribe 0.8-1.2x, overall reaches 1.5-2x oversubscription. If QIBs stay away (<0.5x), red flag for listing performance.

Company Profile: What Does Shree Ram Twistex Actually Do?

Business Model:

Shree Ram Twistex is a B2B (business-to-business) cotton yarn manufacturer based in Gondal, Rajkot, Gujarat. The company does NOT sell directly to consumers — instead, it supplies yarn to:

- Fabric processors

- Textile manufacturers

- Garment exporters

- Bulk buyers for knitting/weaving

Product Portfolio:

| Yarn Type | Description | Applications |

|---|---|---|

| Compact Ring Spun Yarn | Ne 8 to Ne 40 thickness | Denim, terry towels, shirting |

| Carded Yarn | Standard quality cotton | Bottom wear, home textiles |

| Combed Yarn | Premium quality, smoother | Sheeting, premium garments |

| Eli Twist (Siro) Yarn | Twisted for strength | Socks, sweaters, industrial fabrics |

| Compact Slub Yarn | Textured appearance | Fashion fabrics |

| Lycra-Blended Yarn | Elastic properties | Stretch garments, activewear |

Manufacturing Capacity:

- Location: Gondal, Rajkot, Gujarat

- Machines: 17 compact ring-spinning machines

- Installed Capacity: 27,744 spindles

- Technology: Modern compact spinning (produces superior yarn strength and uniformity)

Geographic Reach:

Supplies to customers across:

- Gujarat, Rajasthan, West Bengal, Maharashtra

- Tamil Nadu, Madhya Pradesh, Punjab

- Dadra and Nagar Haveli

Financial Performance: Growth Yes, But Profitability Concerns

| Financial Metric | FY23 | FY24 | FY25 | H1 FY26 | Trend |

|---|---|---|---|---|---|

| Revenue (₹ Lakh) | 18,842 | 23,159 | 25,504 | 13,208 | Growing |

| EBITDA (₹ Lakh) | — | — | — | — | Not disclosed |

| Profit After Tax (₹ Lakh) | 205 | 1,021 | 938 | 700 | Declining |

| EPS (₹) | — | — | 2.72 | — | — |

| Profit Margin % | 1.09% | 4.41% | 3.68% | 5.30% | Volatile |

Critical Financial Observations:

Profit Decline FY24→FY25: PAT fell from ₹10.21 Cr to ₹9.38 Cr despite revenue growth — red flag indicating margin pressure, possibly from rising cotton costs or competition

H1 FY26 Recovery: Profit margin improved to 5.30% (vs 3.68% in FY25) — suggests cost management improving or pricing power returning

Low Absolute Profitability: ₹9.38 Cr profit on ₹255 Cr revenue = 3.68% margin — textile manufacturing is low-margin business vulnerable to input cost volatility

Valuation Analysis:

At ₹104 upper band:

- Market Cap Post-IPO: ~₹360 Crore (estimated)

- P/E Ratio: 38.23x (based on FY25 EPS ₹2.72)

- Comparison: Industry average textile P/E ~18-25x

Verdict: Shree Ram Twistex trades at 50-110% PREMIUM to textile industry average — expensive unless growth accelerates significantly.

Should You Apply? The Bull Case vs Bear Case

BULL CASE (Why Apply):

GMP Momentum: ₹19 GMP suggests 18% listing gain — if sustained, delivers ₹2,736 profit per lot (144 shares)

Renewable Energy Investment: ₹46.85 Cr (47% of funds) into solar/wind will reduce power costs 30-40%, directly boosting margins

Sector Tailwinds: India textile exports targeting $100 billion by FY30, government support via Cotton Mission and PLI schemes

Retail Demand: 95% retail subscription on Day 1 shows genuine grassroots interest

B2B Model: Stable repeat customers (fabric processors, garment exporters) provide revenue visibility

Small Issue Size: Only ₹110 Cr = low supply can create listing day demand surge

BEAR CASE (Why Avoid):

Expensive Valuation: 38x P/E vs industry 18-25x = paying 50-110% premium for a low-margin textile business

Profit Declining: PAT fell FY24→FY25 despite revenue growth = margin pressure visible

Cotton Price Volatility: Single input (cotton) represents 60-70% of costs — any spike crushes margins instantly

Working Capital Intensive: ₹44 Cr (40%) going to working capital = company struggles with cash conversion, needs IPO money to fund operations

Debt Repayment: ₹14.89 Cr (13.5%) for debt repayment = company overleveraged, using IPO to clean balance sheet (red flag)

NII Weakness: HNIs not participating (12% subscription) = sophisticated investors avoiding

No Dividend Policy: Company has NO formal dividend policy = capital appreciation only, but at 38x P/E appreciation requires sustained 25-30% earnings CAGR (unlikely in textiles)

Cyclical Business: Textile demand highly cyclical — economic slowdown = inventory pileup, working capital crunch, margin collapse

Key Takeaways: Shree Ram Twistex IPO Final Day Decision

→ Shree Ram Twistex IPO GMP surges 280% from ₹5 to ₹19 on final subscription day (Feb 25) as issue reaches 75% subscription by Day 2 with strong retail demand (95% subscribed Day 1) — expected listing price ₹123 implies +18.27% gain over ₹104 upper band.

→ Issue fundamentals mixed: 47% of ₹110 Cr going to renewable energy (solar + wind power plants) is positive for long-term cost reduction, but 40% for working capital + 13.5% for debt repayment suggests cash-strapped operations and overleveraged balance sheet.

→ Financial red flags: Profit declined from ₹10.21 Cr (FY24) to ₹9.38 Cr (FY25) despite revenue growth indicating margin pressure; trades at expensive 38x P/E versus textile industry average 18-25x = paying 50-110% premium.

→ Subscription pattern warning: While retail shows 95% enthusiasm, NII (HNIs) at weak 12% subscription signals sophisticated investors avoiding the issue — QIB participation on Day 3 will be critical determinant of listing performance.

→ Bull case for applying: ₹19 GMP momentum + small ₹110 Cr issue size + renewable energy cost-reduction story + retail demand could deliver 15-20% listing gains = ₹2,160-2,880 profit per lot (144 shares).

→ Bear case for avoiding: Expensive 38x valuation + declining profits + cotton price volatility risk + working capital intensive + cyclical textile business + no dividend policy + NII weakness suggests fundamentals don’t justify GMP surge.

→ Final verdict: Apply ONLY if: (1) Can afford to lose ₹14,976 investment, (2) Will exit on listing day regardless of price for 10-18% gain, (3) NOT holding long-term. Avoid if: (1) Looking for quality long-term investment, (2) Risk-averse, (3) Believe fundamentals matter — GMP may be hype-driven and reverse post-listing.

This article is for educational purposes only and does not constitute investment advice. IPO investments involve substantial risk of loss. Always conduct independent research and consult a SEBI-registered advisor before investing.

Data: IPO Watch, Paytm Money, ClearTax, Outlook Money, Business Standard, Groww, StocKart, NewsX as of February 25, 2026.