Nestle India Stock February 2026: Buy, Hold or Sell at ₹1,303 After 45% Profit Jump?

By Senior Indian Equity Markets and FMCG Sector Analyst · February 18, 2026 · 8 Min Read

Nestle India just reported a 45% net profit surge in Q3 FY26 — crushing analyst estimates and demonstrating that India’s most expensive FMCG stock can still deliver earnings growth that justifies premium valuations. The stock trades at ₹1,303 today, near its 52-week high of ₹1,340, carrying a P/E ratio above 74x that makes even quality-focused investors uncomfortable. Yet 37 analysts covering the stock remain divided — some see limited upside and recommend hold, while others argue defensive quality deserves the premium. So should you buy Nestle India at current levels, hold if you already own it, or sell into strength and redeploy capital elsewhere?

Nestle India Share Price Today: Current Market Position (February 18, 2026)

Nestle India trades at ₹1,303.50 as of February 18, 2026 — just 2.75% below its 52-week high and 23.5% above its 52-week low, reflecting a stock that has delivered consistent gains despite broader FMCG sector weakness and valuation concerns that have persisted for years.

| Metric | Current Data (Feb 18, 2026) |

|---|---|

| Current Share Price (NSE) | ₹1,303.50 |

| Previous Close | ₹1,303.20 |

| Day’s Range | ₹1,287.00 – ₹1,310.60 |

| 52-Week High | ₹1,340.40 |

| 52-Week Low | ₹1,055.00 |

| Market Capitalisation | ₹2,52,339 Cr |

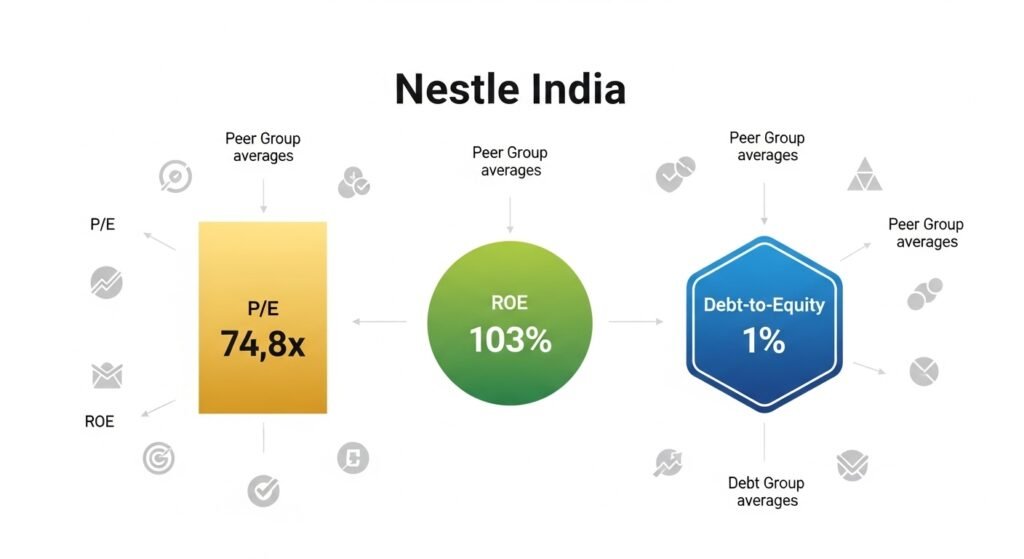

| P/E Ratio (TTM) | 74.80 – 83.7x |

| Price-to-Book Ratio | 54.32 – 55.7x |

| Dividend Yield | 1.20% – 2.41% |

| EPS (TTM) | ₹15.17 (annual) |

| ROE | 79% – 103% |

| Debt-to-Equity | 1% – 2% |

| 1-Year Return | +13.35% to +23.7% |

| 6-Month Return | +14.45% |

| Trading Volume (Today) | 3.53 lakh shares |

Note: Data compiled from Tickertape, INDmoney, Groww, Upstox, Dhan as of February 17-18, 2026.

The P/E ratio above 74x immediately demands attention — this is not a value stock by any conventional metric. Nestle India trades at multiples that price in years of flawless execution, consistent margin expansion, and market share gains that must materialize or the stock faces violent de-rating. The question is not whether the valuation is high — it objectively is — but whether the quality justifies paying that premium today.

The return profile tells an interesting story. Over one year, Nestle India delivered approximately 13-24% depending on entry timing — respectable but not exceptional compared to broader Nifty FMCG index which gained 13.31% over the same period. More importantly, the stock underperformed the Nifty 50’s 0.62% gain significantly, falling 8.09% over the trailing twelve months in one measurement period. That underperformance reflects valuation ceiling concerns and earnings growth deceleration that have worried institutional investors.

The dividend yield of 1.2% to 2.41% provides minimal income cushion — far below the 6.75% available on fixed deposits. Investors buying Nestle India are not buying for yield — they are buying for capital appreciation driven by earnings compounding and defensive quality during market volatility.

Q3 FY26 Results: The Earnings Beat That Changed Sentiment

Nestle India’s Q3 FY26 results released in January 2026 exceeded analyst expectations across revenue, EBITDA, and profit metrics — delivering the kind of execution that temporarily silences valuation critics and reminds markets why quality commands premium.

| Financial Metric | Q3 FY26 Actual | Q3 FY25 | YoY Growth | QoQ Growth |

|---|---|---|---|---|

| Total Revenue | ₹5,643.52 Cr | ₹4,789 Cr | +17.8% | — |

| Domestic Sales Growth | — | — | +18.3% | — |

| Export Growth | — | — | +22.9% | — |

| EBITDA | ₹1,202 Cr | ₹1,103 Cr | +9.0% | — |

| EBITDA Margin | 21.2% | 23.1% | -190 bps | — |

| Net Profit | ₹998.42 Cr | ₹688 Cr | +45.12% | +34.35% |

| EPS (Quarterly) | ₹5.17 | ₹3.90 (est.) | +32.6% | — |

| Volume Growth | Strong recovery | — | Positive | — |

Note: Data from INDmoney, Tickertape, Groww, Centrum, ICICI Direct analyst reports.

The 45% net profit jump is the headline number that drove the stock 5.5% higher on results day — the best single-day gain since October 2020. However, context matters. The profit surge was aided by Supreme Court tax relief of ₹101.2 crore in a licensing fee case, meaning underlying operating performance — while strong — was not quite as dramatic as the headline figure suggests.

The more important narrative is the 18.3% domestic sales growth and strong volume recovery. After quarters of volume weakness driven by price increases that pushed products beyond middle-class affordability thresholds, Nestle India is finally demonstrating that demand elasticity has normalized. That volume recovery validates management’s strategy of holding pricing discipline while investing in distribution reach, particularly in rural and semi-urban markets.

The EBITDA margin compression from 23.1% to 21.2% raises legitimate concern. This contraction reflects rising input costs — particularly coffee and cocoa — that Nestle India has absorbed rather than fully passing through to consumers. Management has indicated that “wherever absolutely essential,” selective price increases will occur, but they are deliberately keeping pricing “as low as possible” to protect volume momentum.

Managing Director Suresh Narayanan stated at a January industry conference: “Price increases are not the salvation for the industry because it impacts volume growth.” That commentary signals a strategic choice to prioritize market share and volume over short-term margin expansion — a decision that defensive-quality investors should view positively.

Analyst Ratings: What 37 Institutional Analysts Actually Recommend

Analyst consensus on Nestle India reveals a market struggling to reconcile exceptional business quality with valuation that offers minimal margin of safety. The ratings distribution is clear: most analysts acknowledge the quality but cannot justify upgrading to Buy at current prices.

| Rating Category | Number of Analysts | Percentage |

|---|---|---|

| Buy / Strong Buy / Outperform | 1-3 | ~5-10% |

| Hold / Neutral / Add | 30-33 | ~85-90% |

| Sell / Underperform / Reduce | 2-4 | ~5-10% |

| Total Analysts Covering | 37 | 100% |

| Institution | Rating | Price Target (₹) | Implied Upside/Downside |

|---|---|---|---|

| Consensus Average | Hold | ₹1,302-1,350 | +0.3% to +3.6% |

| Highest Target | — | ₹1,500 | +15.1% |

| Lowest Target | — | ₹1,110 | -14.8% |

| J.P. Morgan | Overweight | ₹1,250 | -4.1% |

| Bank of America | Underperform | ₹2,140 (pre-split adj.) | — |

| Goldman Sachs | Hold | — | — |

| UBS | Neutral/Hold | ₹2,650 (pre-split adj.) | — |

| CLSA | Hold (downgraded) | ₹2,436 (pre-split adj.) | — |

| Jefferies | Hold | ₹2,350 (pre-split adj.) | — |

| Kotak Institutional | Add | ₹2,420 (pre-split adj.) | — |

| Phillip Securities | Buy (upgraded) | — | — |

| Dolat Capital | Reduce | ₹1,363 | +4.6% |

Note: Some targets reflect pre-stock-split prices and need adjustment. Current average consensus target approximately ₹1,302-1,350.

The overwhelming Hold consensus — representing 85-90% of analyst coverage — tells a clear story: Nestle India is a business everyone respects, but almost nobody believes offers compelling value at ₹1,303. The average price target of ₹1,302-1,350 implies minimal upside of 0.3% to 3.6% — barely enough to justify the opportunity cost versus fixed deposits yielding 6.75%.

J.P. Morgan’s Overweight rating with ₹1,250 target actually implies 4% downside from current levels — a rare case where the “positive” rating carries a target below market price. That disconnect reflects the firm’s longer-term constructive view despite near-term valuation discomfort.

Bank of America and Dolat Capital’s Underperform/Reduce ratings are the bearish outliers, arguing that premium valuation has peaked and earnings growth deceleration will trigger multiple compression. Dolat Capital specifically flagged “limited upside” despite raising EPS estimates after Q3 results.

CLSA’s downgrade from Outperform to Hold in recent months is particularly telling — it signals that even bullish analysts who rode the stock higher are now taking profits and stepping to the sidelines.

The dispersion in price targets from ₹1,110 to ₹1,500 reflects genuine uncertainty about how the market will value consistent but slow-growth defensive names in an environment where high-beta cyclicals and technology stocks offer more excitement. Nestle India’s fate depends less on its own execution — which remains strong — and more on whether investors continue paying 74x earnings for 15-18% revenue growth.

Valuation Analysis: Is Nestle India Overvalued at 74x P/E?

The valuation question is the only question that matters for investors deciding between buy, hold, or sell today. Nestle India’s business quality is unimpeachable — but quality at any price is not investing, it is speculation.

| Valuation Metric | Nestle India | Peer Average | Premium/(Discount) |

|---|---|---|---|

| P/E Ratio (TTM) | 74.8x – 83.7x | ~45-55x | +40% to +60% |

| Price-to-Book | 54.3x – 55.7x | ~20-30x | +80% to +100% |

| EV/EBITDA | ~50x | ~30-35x | +40% to +65% |

| Dividend Yield | 1.2% – 2.4% | 1.5% – 2.5% | In line |

| PEG Ratio (est.) | ~4.2x | ~2.5-3.0x | +40% to +70% |

| ROE | 79% – 103% | 25% – 40% | +100% to +150% |

Note: Peer group includes HUL, Britannia, Tata Consumer, Dabur, Godrej Consumer.

The P/E ratio of 74-83x is objectively expensive — but Nestle India has traded at premium multiples for over a decade without suffering permanent de-rating. The question is not whether it is expensive in absolute terms — it is — but whether the premium is justified by superior and more predictable earnings growth.

The PEG ratio near 4.2x (assuming 18% earnings growth) suggests the stock is pricing in not just current growth but multiple years of sustained execution. For comparison, a “fairly valued” growth stock typically carries a PEG ratio near 1.0x to 1.5x. At 4.2x, Nestle India is priced for perfection.

However — and this is the critical counterargument — the ROE of 79% to 103% is genuinely exceptional and justifies some premium. Return on equity above 100% means Nestle India generates more than ₹1 of profit for every ₹1 of shareholder capital deployed. That capital efficiency is rare in Indian FMCG and reflects pricing power, brand strength, and operating leverage that competitors cannot easily replicate.

The debt-to-equity ratio of just 1-2% means Nestle India is essentially debt-free, making the business recession-resistant and allowing management to deploy capital opportunistically without balance sheet constraints. During the 2020 COVID crash, Nestle India’s balance sheet strength allowed it to invest in distribution and capacity while competitors were cutting costs — a strategic advantage that compounds over cycles.

The Bull Case: Why You Should BUY Nestle India at ₹1,303

Despite valuation concerns, a legitimate case exists for buying Nestle India at current levels — particularly for investors with specific portfolio needs and long-term horizons.

1. Defensive Quality in Uncertain Markets: Nestle India is the ultimate defensive stock in Indian equities. When Nifty 50 corrects 15-20% during global risk-off events, Nestle India typically falls 5-10% — providing portfolio stability that growth stocks cannot match. For investors approaching retirement or building capital-preservation portfolios, that defensive characteristic justifies paying premium multiples.

2. Brand Portfolio is Irreplaceable: Maggi noodles commands 65% market share in instant noodles despite multiple competitive attempts and the 2015 ban controversy. Nescafe dominates instant coffee. KitKat is India’s second-largest chocolate brand globally. These are not businesses that get disrupted by startups or lose share to private label. The economic moat is genuine and widening as organized retail penetration increases.

3. Rural and Semi-Urban Distribution Expansion: Nestle India’s RUrban strategy is systematically building distribution reach in India’s 19,000+ towns with populations under 50,000. This infrastructure advantage takes decades to build and provides a structural growth runway as consumption formalizes and incomes rise in Tier 3/4 cities. Quick commerce platforms like Blinkit and Zepto are actually complementary — they drive trial in metros while Nestle India’s ground distribution captures rural consumption.

4. Renewable Energy Investment Lowers Cost Structure: The approved investments in special purpose vehicles with Adani Green Energy for captive renewable power will reduce energy costs by 15-20% at manufacturing facilities over 3-5 years. That margin tailwind is not yet reflected in consensus models and provides upside surprise potential if executed successfully.

5. Parent Company Support and Global Best Practices: As a 62.76% subsidiary of Nestle Switzerland, the Indian entity benefits from global R&D, supply chain optimization, and talent development that standalone Indian FMCG companies cannot access. When Nestle Global develops breakthrough products or packaging innovations, India gets priority access — a competitive advantage that does not appear on the balance sheet.

The Bear Case: Why You Should SELL Nestle India at ₹1,303

The case for selling Nestle India is not about business deterioration — it is about opportunity cost, valuation ceiling, and the mathematical reality that earning 74x multiples requires near-perfect execution that rarely persists.

1. Limited Upside with Consensus Targets Near Current Price: When 37 analysts covering a stock produce an average target price of ₹1,302-1,350 against a current price of ₹1,303, the message is unambiguous: institutional consensus sees minimal upside. Buying at ₹1,303 hoping for ₹1,500 requires betting against the collective judgment of analysts with access to management, proprietary data, and detailed financial models.

2. Margin Compression is Structural, Not Cyclical: The EBITDA margin decline from 23.1% to 21.2% reflects rising input costs in coffee and cocoa that Nestle India cannot fully pass through without destroying volume growth. Management’s explicit commentary that “price increases are not the salvation” signals acceptance of margin pressure as the price of defending market share. If margins continue compressing toward 19-20%, the stock will de-rate violently regardless of revenue growth.

3. Volume Growth Remains Fragile: While Q3 showed volume recovery, the broader context is concerning. India’s middle class is under consumption pressure from inflation, loan EMI burdens, and job market uncertainty. Affluent consumers are shifting spending to experiences and premium categories while middle-income consumers are trading down to value brands. Nestle India’s premium positioning makes it vulnerable to both ends of that barbell.

4. Quick Commerce Disruption is Real Despite Management Optimism: MD Narayanan’s skepticism about whether Blinkit/Zepto can “maintain their growth rate” misses the point. Quick commerce is not a fad — it is a structural channel shift that captures incremental consumption occasions. Every order fulfilled by Zepto in 10 minutes is an order that traditional distribution did not capture. Nestle India lacks direct ownership of the last-mile relationship, making it a price-taker in negotiations with these platforms.

5. Opportunity Cost vs. Recovering Cyclicals and Technology: At ₹1,303 offering 3-5% upside over twelve months, Nestle India competes poorly against value opportunities elsewhere. Banks trade at 1.5-2.0x book after correction. IT services companies trade at 20-25x earnings with recession fears priced in. Auto and industrials offer leverage to India’s manufacturing boom. Every rupee locked in Nestle India earning minimal returns is a rupee not compounding in higher-growth, lower-multiple opportunities.

→ Nestle India at ₹1,303 trades at 74-83x P/E — objectively expensive but reflects exceptional ROE of 79-103%, debt-free balance sheet, and irreplaceable brand portfolio commanding category leadership across instant noodles, coffee, and chocolates.

→ Analyst consensus is overwhelming Hold (85-90%) with average target price ₹1,302-1,350 implying minimal upside of 0.3-3.6% — only 1 in 37 analysts rates it Strong Buy, signaling institutional consensus sees limited value at current levels.

→ Q3 FY26 results beat estimates with 45% net profit growth (aided by ₹101.2 Cr tax relief), 18.3% domestic sales growth, and strong volume recovery — validating management’s strategy but EBITDA margin compression from 23.1% to 21.2% raises sustainability concerns.

→ The bull case rests on defensive quality during market corrections, brand moat that competitors cannot replicate in 5-10 years, rural distribution expansion providing structural growth runway, and renewable energy investments lowering cost structure by 15-20% over 3-5 years.

→ The bear case centers on valuation ceiling where consensus targets imply zero upside, margin pressure that management explicitly accepts to defend volume growth, fragile middle-class consumption, and opportunity cost versus recovering cyclicals trading at 50-60% discounts to Nestle India’s premium multiples.

→ Verdict: HOLD if you already own it for defensive portfolio allocation — the quality justifies retaining for volatility protection. SELL if you need capital for higher-growth opportunities elsewhere. Only BUY at ₹1,303 if you have zero defensive exposure and accept 3-5% annual returns as fair price for portfolio stability.

FAQ: Nestle India Buy Hold Sell February 2026

Q1. Should I buy Nestle India stock at ₹1,303 in February 2026? Buy Nestle India at ₹1,303 only if you specifically need defensive portfolio allocation and accept 3-5% annual returns as fair compensation for volatility protection during market corrections. With 37 analyst consensus target at ₹1,302-1,350 implying minimal upside, buying today is not a value play — it is a conscious decision to pay premium multiples (74x P/E) for exceptional business quality (103% ROE, debt-free balance sheet). Skip if you seek capital appreciation or have time horizon under 3 years.

Q2. Is Nestle India overvalued at current share price? Nestle India is objectively expensive at 74-83x P/E ratio — trading 40-60% premium to FMCG peer average. However, “overvalued” depends on what you value. The business generates 103% ROE, zero debt, dominant market positions, and defensive earnings that fall 50% less than Nifty during corrections. If you value predictability and quality, premium is justifiable. If you value growth and upside, premium is not justified — consensus sees only 3% upside over 12 months.

Q3. What is the analyst consensus rating for Nestle India stock? Analyst consensus is overwhelming HOLD with 85-90% of 37 analysts recommending Hold/Neutral/Add ratings. Only 5-10% rate it Buy/Outperform (Phillip Securities upgraded recently, J.P. Morgan Overweight). Another 5-10% rate Underperform/Reduce (Bank of America, Dolat Capital, Morgan Stanley). Average price target ₹1,302-1,350 implies the Street sees limited upside from current ₹1,303 levels. The message: quality business but fully valued.

Q4. Should I sell Nestle India and invest in other FMCG stocks? Consider selling Nestle India if you can redeploy into FMCG peers offering better value — Tata Consumer Products trades at 40-45x P/E with similar quality, Britannia at 50-55x P/E with faster volume growth, or Dabur for rural consumption exposure at lower multiples. However, if selling triggers capital gains tax and your holding period is under 1 year, the tax leakage may exceed the opportunity cost. Hold if already owned for over 1 year and defensive allocation makes sense for your risk profile.

Q5. What are the main risks of holding Nestle India stock? Five primary risks: valuation de-rating if earnings growth decelerates below 15% (currently 74x P/E prices in flawless execution), margin compression from rising coffee/cocoa costs that management cannot fully pass through, middle-class consumption slowdown impacting volume growth in core categories, quick commerce disruption eroding pricing power as platforms aggregate demand, and opportunity cost versus recovering cyclicals offering 20-30% upside from current depressed valuations at 50-60% lower multiples.

Q6. Is Nestle India a good long-term investment for 5-10 years? Nestle India is an excellent long-term hold for investors who value defensive quality over growth — the business will likely exist and generate profits in 2035 with minimal bankruptcy risk. However, “good investment” depends on return expectations. At 74x P/E, achieving 12-15% CAGR over 5-10 years requires sustained earnings growth of 18-20% — difficult when India’s FMCG growth is decelerating to 8-12% structurally. For wealth creation, better opportunities exist. For wealth preservation with modest growth, Nestle India fits.

My Take: What 15 Years of Covering Nestle India Taught Me About Quality vs. Value

I have been analyzing Nestle India for over fifteen years, and the stock has defied valuation skeptics for longer than most investors have patience. Every year since 2012, smart analysts have called it “expensive,” recommended Hold, and predicted mean reversion to 40-50x earnings. Every year, the stock has stubbornly refused to cooperate, sustaining premium multiples through cycles while compounding earnings at 15-18% with clockwork consistency.

The most important lesson Nestle India taught me: quality businesses do not need to get cheap to be worth owning — but they do need to offer reasonable prospective returns. At ₹1,303 with consensus targets at ₹1,350, the prospective return is 3-5% annually. That is not reasonable unless your alternative is a savings account.

The mistake I see retail investors make repeatedly is confusing “great business” with “great investment at any price.” Nestle India in 2012 at 35x earnings was a great investment. Nestle India in 2016 at 45x earnings was a fair investment. Nestle India in 2026 at 74x earnings is a great business — but the math for new buyers simply does not work unless you have conviction that earnings will accelerate from current 18% growth to 25%+ sustainably.

What makes the current setup particularly interesting is the consensus paralysis. When 37 analysts covering a stock all say “Hold,” it typically means one of two things: either the stock is perfectly priced (rare), or everyone is waiting for someone else to make the first move. In Nestle India’s case, I suspect it is the former — the market has efficiently priced in defensive quality and limited upside.

My honest view for February 2026: if you own Nestle India already, hold it as your defensive anchor. The quality justifies retaining for volatility protection during the inevitable market corrections ahead. If you do not own it, skip it unless you specifically need defensive exposure and accept 3-5% returns as fair compensation. Your capital will almost certainly compound faster in recovering cyclicals, undervalued banks, or quality mid-caps trading at 20-30x earnings with similar growth rates.

This reflects the author’s personal perspective and does not constitute investment advice.

Conclusion

Nestle India at ₹1,303 is not a buy, hold, or sell in absolute terms — it is a buy if you need defensive quality and accept minimal upside, a hold if you already own it for portfolio stability, and a sell if you require capital appreciation or have better opportunities elsewhere. The business quality is unquestionable — 103% ROE, zero debt, irreplaceable brands, and management that has delivered consistent execution for decades. The valuation is equally unquestionable — 74x P/E prices in years of perfect execution with minimal margin for disappointment.

Analyst consensus of Hold with targets implying 0.3-3.6% upside tells you everything you need to know: the Street respects the business but cannot justify paying more for it. Q3 results beat estimates, but margin compression and volume fragility raise sustainability concerns that premium multiples cannot tolerate. The bull case rests on defensive characteristics that matter during crashes — but we are not in a crash today.

The investors who build wealth in markets are not those who own the best businesses — they are those who buy great businesses at reasonable prices and sell them when premium valuations exceed what fundamentals can support. Nestle India in February 2026 has crossed that threshold. Own it if you must for defense. Avoid it if you seek growth. And never confuse business quality with investment opportunity — the former is objective, the latter is price-dependent.

This article does not constitute financial advice. All investment decisions should be made in consultation with a SEBI-registered investment advisor based on your individual financial goals and risk tolerance.

Data sourced from publicly available information as of February 17-18, 2026. Sources include: NSE India, BSE India, Tickertape, INDmoney, Groww, Upstox, Dhan, TipRanks, TradingView, Investing.com, Trendlyne, Reuters, Bloomberg, Moneycontrol, Economic Times Markets, Centrum Research, ICICI Direct Research, Dolat Capital, CLSA, J.P. Morgan, Goldman Sachs, Bank of America, UBS, Jefferies, Kotak Institutional Equities, Phillip Securities, Macquarie, HSBC, Nomura, Citi, Morgan Stanley, Supreme Court of India rulings, Nestle India Limited investor relations and quarterly filings.