HDFC Bank Share Price March 2026: The ₹821.50 Capitulation — Why India’s Private Banking King Hit 52-Week Low Despite 12% Profit Growth and What the ₹1,050 Kotak Target Really Means

By Senior Private Banking Sector, Deposit Wars and Post-Merger Integration Analyst · March 10, 2026

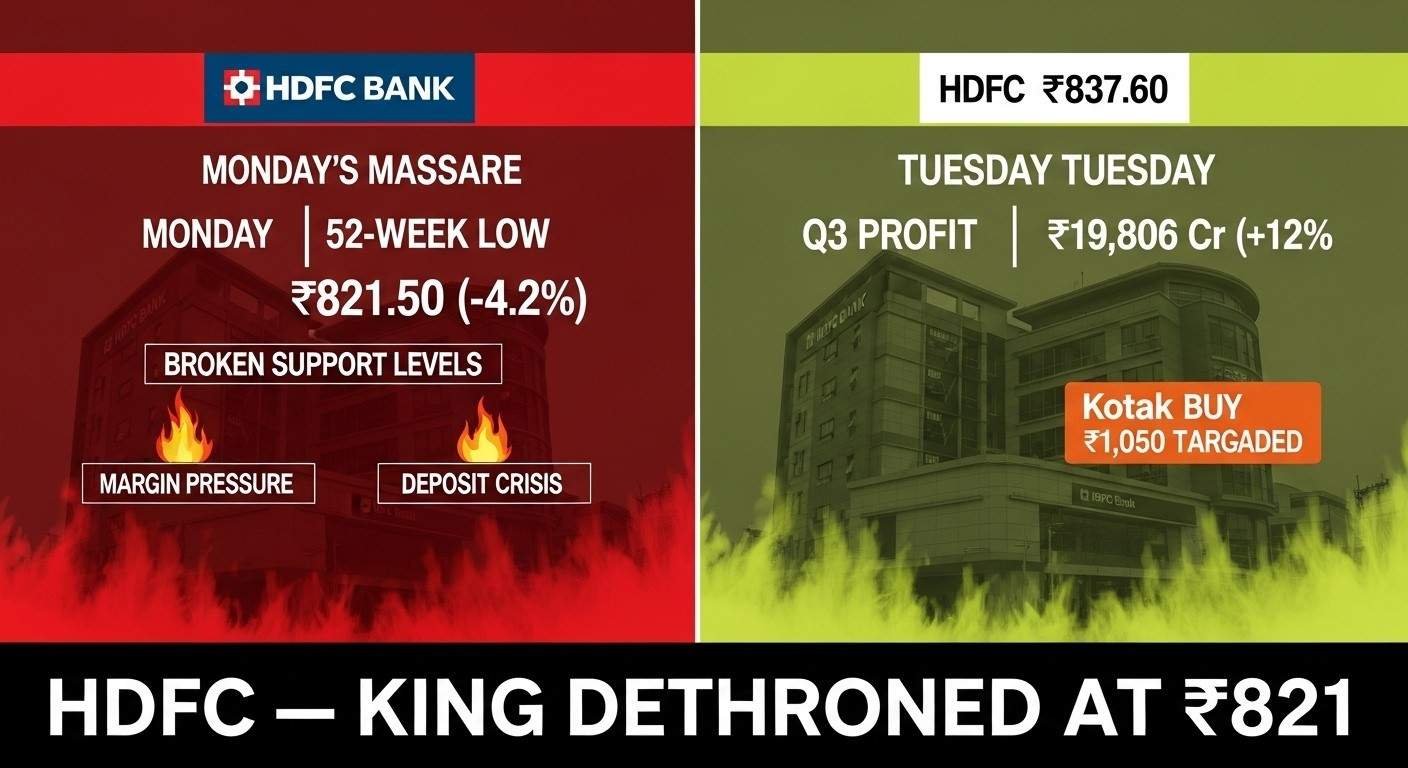

HDFC Bank, once the undisputed king of Indian private sector banking commanding premium valuations and investor loyalty for over two decades, finds itself in the most humiliating position of its storied history on Tuesday March 10, 2026 trading at ₹837.60 after Monday’s catastrophic crash to a fresh fifty two week low of ₹821.50 that represents an eighteen percent decline from the ₹1,020.50 high achieved just weeks ago and leaves the bank’s thirteen lakh nineteen thousand crore rupee market capitalization vulnerable to further erosion if the Iran war-driven volatility persists. This dramatic fall from grace comes despite third quarter fiscal 2026 results showing net profit surging twelve point one eight percent year-over-year to nineteen thousand eight hundred six point six three crore rupees, creating one of the most confusing disconnects between fundamental performance and stock price action that veteran banking analysts have witnessed in years.

The central mystery confronting HDFC Bank’s seven crore ninety two lakh shareholders Tuesday morning is how a bank that reported steady profit growth, maintains the largest deposit franchise among private banks with market-leading customer satisfaction scores, and just received a rating upgrade from Kotak Institutional Equities to Buy with a ₹1,050 price target citing valuation discount, can simultaneously be trading below ₹840 after getting crushed in Monday’s session that saw one point one seven crore shares trade hands worth ninety seven thousand eighty one lakh rupees as investors fled en masse. Understanding this paradox requires looking beyond quarterly earnings headlines to the deeper structural issues around net interest margin compression from three point one five to three point one two percent, aggressive competition for deposits that HDFC is losing to nimbler rivals, and post-merger integration challenges with parent HDFC Ltd that are taking longer to resolve than management anticipated.

Monday’s 52-Week Low Disaster: The Numbers Behind the Carnage

Let me reconstruct exactly what happened to HDFC Bank shares during Monday March ninth’s trading session because the magnitude of destruction provides crucial context for understanding whether Tuesday’s modest recovery to ₹837.60 represents genuine stabilization or merely a temporary pause before deeper declines toward ₹780 to ₹800 territory that some technical analysts now warn could materialize if crude oil sustains above one hundred dollars per barrel. Monday opened with HDFC gapping down dramatically to ₹825.00 from Friday’s close of ₹857.05, representing a thirty two point zero five rupee or three point seven four percent overnight evaporation of shareholder wealth that instantly established the session’s bearish tone.

But that opening gap-down proved to be just the beginning of Monday’s nightmare. Rather than finding value buyers at these depressed levels who might view the dip as opportunity to accumulate India’s second largest private bank at attractive valuations, selling pressure actually accelerated throughout the morning session. By late morning around eleven AM, HDFC had crashed through ₹825 support to test ₹822. The intraday low of ₹821.50 came around midday, representing a devastating thirty five point five five rupee decline from Friday’s close or four point one five percent intraday crash that marked the absolute lowest price HDFC Bank has traded in the past fifty two weeks, breaking below the previous low and establishing new bearish territory.

The stock managed only modest recovery from that intraday abyss to close Monday at ₹829.40, still down twenty seven point six five rupees or three point two three percent for the session. This closing price had enormous psychological implications beyond just the percentage decline. First, it confirmed the fifty two week low at ₹821.50 as a legitimate bottom test rather than just a brief intraday spike down. Second, it left HDFC trading decisively below the psychologically critical ₹860 level that had acted as support multiple times in recent weeks. Third, it pushed the stock below all major moving averages including five-day, twenty-day, fifty-day, one hundred-day, and two hundred-day, creating what technical analysts call a death cross pattern that typically signals extended downtrends.

The volume statistics from Monday’s session tell their own story of capitulation. One point one seven crore shares changed hands worth approximately ninety seven thousand eighty one lakh rupees, representing significantly elevated activity compared to normal daily volumes. This heavy volume on a down day suggests distribution rather than accumulation, meaning large holders were selling aggressively rather than buyers stepping in to support the stock. The delivery volume of two point four seven crore shares on March sixth that preceded Monday’s crash was ten point five seven percent higher than the five day average, indicating rising investor participation but unfortunately that participation was dominated by sellers rather than buyers.

Tuesday’s Dead Cat Bounce or Real Recovery

Tuesday March tenth brought the market-wide relief rally driven by crude oil’s collapse from one hundred eighteen dollars to eighty eight dollars and President Trump’s signals that the Iran war may end soon, and HDFC Bank participated in this sector-wide bounce though with far less enthusiasm than aviation or automobile stocks that benefited more directly from lower oil prices. HDFC opened Tuesday higher though exact opening data varies across sources, with midday trading showing the stock at ₹837.60 representing a gain of approximately eight point two rupees or one percent from Monday’s close around ₹829.

The intraday high Tuesday reached ₹839.70, briefly pushing the stock toward the psychologically important ₹840 to ₹850 range before profit-taking emerged and pushed prices back toward ₹837 to ₹838. This failure to sustain gains above ₹840 despite the broader market rally is concerning because it suggests HDFC-specific issues are weighing on the stock beyond just the general market volatility. While Nifty and Sensex recovered one to two percent from Monday’s lows, HDFC’s one percent gain was underwhelming and left the stock still dramatically below Friday’s ₹857 close, meaning the cumulative two-day performance from Friday through Tuesday still shows a net loss of approximately twenty rupees or two point three percent.

The critical question investors must answer Tuesday afternoon and Wednesday morning is whether this represents genuine bottoming at ₹821.50 with recovery beginning, or merely a classic dead cat bounce where markets briefly rally before resuming the downtrend toward deeper lows. Several factors suggest caution despite Tuesday’s relief. The stock remains eighteen percent below its fifty two week high of ₹1,020.50, still trades below the ₹860 resistance level that now acts as formidable overhead supply, and shows no technical reversal patterns that would confirm a bottom. The elevated India VIX above twenty three despite falling from Monday’s twenty four point four nine indicates continued market uncertainty that could trigger renewed selling if any negative catalysts emerge.

The Margin Pressure Crisis That Nobody Wants to Discuss

The fundamental reason HDFC Bank stock cannot hold ₹900 despite reporting twelve percent profit growth comes down to a three-letter acronym that strikes fear in the hearts of banking investors: NIM, or net interest margin. This metric represents the difference between what a bank earns on its loans and what it pays on its deposits, and it is the single most important driver of banking profitability. HDFC’s NIM compressed from three point one five percent in the December 2024 quarter to three point one two percent in the December 2025 quarter, representing a three basis point decline that might sound trivial but translates to hundreds of crores in lost annual profit when applied across HDFC’s multi-lakh crore loan book.

The margin compression reflects a brutal competitive reality in Indian banking circa March 2026: deposits have become the scarce resource that determines which banks can grow and which must shrink. Every bank from State Bank of India to small finance banks is competing aggressively for household savings by offering higher interest rates on fixed deposits and savings accounts. HDFC has been forced to increase deposit rates to attract and retain funds, but it cannot raise loan rates proportionally because corporate borrowers and retail customers have multiple options and will simply switch to competitors offering better terms. This vise between rising deposit costs and stagnant loan yields is squeezing margins relentlessly.

The problem is structural rather than cyclical, meaning it won’t resolve when the Iran war ends or when markets stabilize. The post-merger integration with parent HDFC Ltd has created a massive liability franchise that requires continuous deposit mobilization to fund the enlarged balance sheet. HDFC Bank is no longer the nimble private sector player that could cherry-pick the best customers and maintain premium margins. It is now a behemoth competing directly with State Bank of India for market share, and that competition forces margin compression toward industry averages rather than maintaining premium spreads.

Industry analysts watching the deposit wars closely estimate that HDFC will need to mobilize approximately fifteen to twenty lakh crore rupees in additional deposits over the next two to three years to fund projected loan growth and maintain regulatory capital adequacy ratios. That deposit mobilization will require offering competitive or above-market interest rates, which mathematically means further margin compression is likely inevitable. The market is forward-looking and pricing in the possibility that HDFC’s NIM could fall from current three point one two percent toward three percent or even two point nine percent over the next four to six quarters, which would devastate earnings growth despite volume expansion.

The Kotak Buy Rating: Hope or False Signal

Amid the carnage of HDFC’s crash to ₹821.50, one piece of positive news emerged that gave bulls something to cling to: Kotak Institutional Equities upgraded HDFC Bank to Buy rating with a ₹1,050 price target, citing valuation discount as the primary rationale. This target represents twenty five percent upside from Tuesday’s ₹837 price and would represent genuine recovery toward the ₹1,000-plus levels that HDFC traded at just weeks ago. The question investors must ask is whether Kotak’s bullish call represents genuine analytical insight or whether it is simply catching a falling knife based on traditional valuation metrics that no longer apply in the post-merger deposit-constrained banking environment.

The bull case that Kotak and other optimistic analysts present goes something like this: HDFC Bank at ₹837 trades at a price-to-earnings ratio of just eighteen point six nine times trailing twelve months earnings and a price-to-book value of two point five times, both representing significant discounts to historical averages and peer valuations. HDFC historically commanded PE ratios of twenty two to twenty five and price-to-book of three to three point five based on its superior return on equity, deposit franchise quality, and management execution. If those historical multiples were applied to current earnings, the stock should trade at ₹1,100 to ₹1,200 rather than ₹837, suggesting forty to fifty percent upside from current depressed levels.

Furthermore, the analysts point to HDFC’s fundamental strengths that remain intact despite stock price weakness: market capitalization still ranks it among India’s top three private banks at ₹13.19 lakh crore, annual sales of ₹3.08 lakh crore represent nearly one-third of the private banking industry’s total revenue underscoring dominant market position, return on assets at one point eight percent demonstrates consistent profitability, capital adequacy ratio of seventeen point two nine percent provides robust buffer against credit risks, and net profit growth of nineteen point six percent annually over medium term reflects healthy earnings trajectory. These metrics support the argument that current stock price represents temporary market dislocation rather than permanent impairment of franchise value.

The bear case against Kotak’s ₹1,050 target is equally compelling and explains why the stock trades at ₹837 despite those seemingly attractive fundamentals. Bears argue that historical valuation multiples were appropriate when HDFC was a growth story with expanding margins and market share gains, but the post-merger reality is a mature franchise facing margin compression and deposit market share losses to more aggressive competitors. They point to HDFC’s underperformance versus BSE500 over the last three years, one year, and three months as evidence that the market has already repriced the stock to reflect this new reality. The Mojo Score of just fifty one point zero and Hold grade despite recent upgrade from Sell suggests even quantitative models struggle to justify bullish positioning.

Most damagingly, bears note that every previous analyst upgrade and buy rating over the past six months has been followed by further stock price declines, creating a pattern where traditional fundamental analysis keeps getting blindsided by the structural headwinds that quarterly earnings reports don’t fully capture. The technical chart showing the stock trading below all moving averages and printing fresh fifty two week lows suggests the market knows something that the analysts’ spreadsheet models don’t, and fighting that tape by buying on valuation typically ends badly.

What Investors Should Actually Expect This Week

Your HDFC Bank investment decision Wednesday and beyond depends entirely on whether you believe the ₹821.50 Monday low represents capitulation marking a tradable bottom, or whether it is merely a way station on a longer journey toward ₹780 to ₹750 if the structural margin pressure and deposit competition issues prove more severe than currently priced in. Let me provide specific frameworks for different scenarios and investor types to help navigate this uncertainty.

If you currently own HDFC Bank purchased at ₹900 to ₹1,020 during recent months and are sitting on losses of thirteen to twenty two percent, Wednesday requires brutal honesty about your thesis. If you bought HDFC based on historical brand strength and reputation without understanding the post-merger challenges and margin dynamics, accept the lesson and exit on any bounce to ₹860 to ₹880 rather than hoping for full recovery. The market is telling you that HDFC at ₹1,000-plus was overvalued for the new competitive reality. If you bought based on fundamental research understanding the deposit challenges but believing management could navigate them successfully, averaging down at ₹820 to ₹840 with a three to five year horizon makes sense, but only if you genuinely have conviction and capital to tolerate further downside to ₹750.

If you are fortunate enough to have bought HDFC at ₹650 to ₹750 during 2024 and 2025 and are sitting on gains of twelve to twenty nine percent despite recent weakness, Wednesday is a day for profit-taking discipline. Book thirty to forty percent of your position at ₹840 to ₹860 if the stock reaches those levels to lock in gains. Trail a stop loss on remaining sixty to seventy percent at ₹800 to protect against catastrophic decline below ₹780. Do not get greedy hoping to recapture ₹1,000-plus highs when the fundamental picture has changed so dramatically.

If you are sitting in cash considering fresh purchase of HDFC Bank, Wednesday requires patience rather than action. The ₹821.50 Monday low might represent the bottom, but confirmation is needed before committing capital. Wait for the stock to reclaim and hold ₹880 to ₹900 for at least two consecutive sessions before buying twenty to thirty percent of intended allocation. If the stock breaks below ₹820 and falls to ₹780 to ₹800, that becomes the next potential entry point for another thirty percent deployment. Keep final forty percent in reserve for even lower levels or for adding if the stock breaks above ₹950 confirming recovery.

For traders rather than investors, HDFC’s range appears to be ₹820 to ₹880 for the March expiry period. Buy near ₹820 to ₹830 with tight stop below ₹810, target ₹860 to ₹880 for exit. Sell near ₹870 to ₹880 with stop above ₹890, target ₹830 to ₹840. This is not a high-conviction trending trade, it is range-bound mean reversion that requires perfect execution and discipline to avoid whipsaw losses.

The brutal reality is that HDFC Bank at ₹837 represents a fundamentally solid bank trading at reasonable valuations temporarily depressed by geopolitical chaos, but also a franchise facing structural headwinds that make quick recovery to ₹1,000-plus unlikely. Expect continued volatility, respect the technical breakdown, and position accordingly based on your genuine conviction about whether management can solve the deposit mobilization and margin pressure challenges over the coming quarters.

This article is for educational purposes only and does not constitute investment advice. Banking stocks remain volatile during margin compression and geopolitical crises. All investment decisions should be made based on individual financial circumstances and risk tolerance.