TCS Share Price Feb 2026: ₹2,686 After 14% Profit Drop — Buy or Sell?

TCS Share Price February 2026: Down 31% from Peak at ₹2,686 After 14% Profit Drop — But $1.8 Billion AI Revenue Changes the Narrative

By Senior Indian Technology Sector and Equity Markets Analyst · February 24, 2026 · 10 Min Read

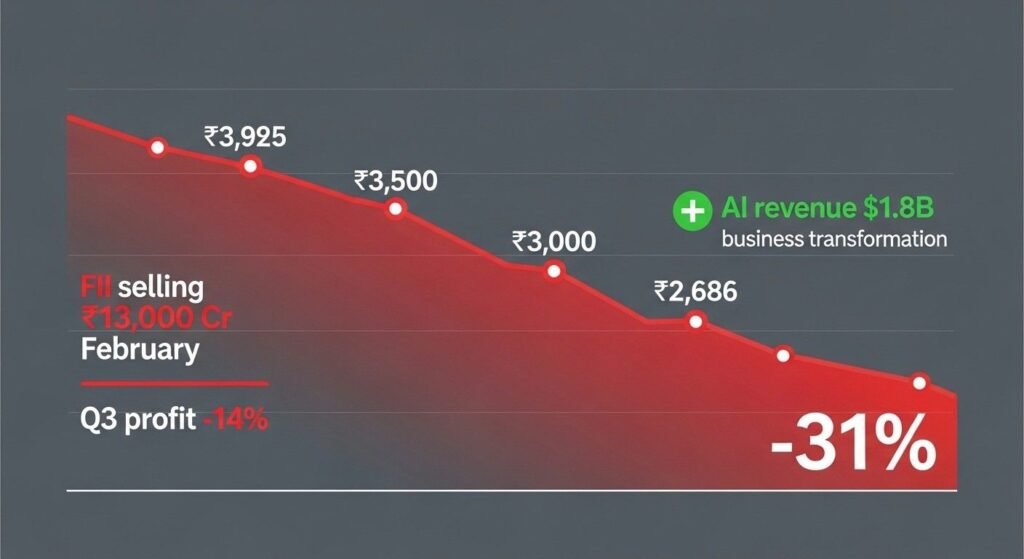

Tata Consultancy Services trades at ₹2,686 on Monday, February 24, 2026 — a staggering 31% below its ₹3,925 52-week high reached just months ago, marking one of the deepest corrections in Indian large-cap IT stocks this cycle. The selloff accelerated after Q3 FY26 results showed net profit crashing 14% YoY to ₹10,657 crore despite 4.9% revenue growth, driven by restructuring costs, new labour code impacts, and headcount reduction of 11,151 employees. Yet beneath the carnage lies a transformative shift: TCS’s AI services revenue hit $1.8 billion annualized (+17.3% QoQ in constant currency), OpenAI partnership secured for the new Hypervault data center, and Morgan Stanley maintaining Overweight with ₹3,540 target (+32% upside). So is TCS at ₹2,686 a generational buying opportunity in India’s most valuable IT company — or a value trap as structural demand weakness destroys the bull thesis?

TCS Share Price Today: The Brutal 31% Correction from ₹3,925 Peak

TCS’s position at ₹2,686 represents not just a routine correction but a violent re-pricing of the entire Indian IT services sector as investors flee growth-at-any-price narratives and demand evidence that AI investments translate to sustainable profitability.

| Metric | Current Data (Feb 20-24, 2026) |

|---|---|

| Current Share Price | ₹2,677 – ₹2,728 |

| Previous Close (Feb 20) | ₹2,685.90 |

| Day’s Range | ₹2,673 – ₹2,741 |

| 52-Week High | ₹3,924.40 – ₹4,139.50 |

| 52-Week Low | ₹2,585 – ₹2,866 |

| From 52-Week High | -31.5% to -35.1% |

| From 52-Week Low | +3.5% to +5.4% |

| Market Capitalisation | ₹9,68,887 – ₹9,83,179 Cr |

| P/E Ratio (TTM) | 20.08 to 21.20 |

| Price-to-Book Ratio | 9.1 to 11.51 |

| EPS (Q3 FY26) | ₹29.45 (quarterly) |

| EPS (FY25 Annual) | ₹134.19 |

| Book Value Per Share | ~₹264 |

| Dividend Yield | 4.03% – 4.68% |

| 1-Year Return | -18.6% to -23% |

| 6-Month Return | -14.8% |

| Trading Volume | 10-84 lakh shares |

Note: Data from Tickertape, Yahoo Finance, 5paisa, INDmoney, Dhan, Kotak Neo as of February 19-24, 2026.

The 31-35% drawdown from the ₹3,925-4,140 peak to current ₹2,686 has erased approximately ₹3.5 lakh crore in market capitalization — more than the entire market cap of companies like Asian Paints or Bajaj Finance. That magnitude of value destruction in India’s second-most valuable company (after Reliance) signals systematic repricing, not temporary volatility.

The stock now trades just 3.5-5.4% above its 52-week low near ₹2,585 — a level that previously represented “crisis pricing” during peak FII selling in IT stocks. The fact that TCS bounced only marginally from that low despite strong Q3 revenue growth and AI momentum suggests deep skepticism about the sector’s near-term trajectory.

Q3 FY26 Results: The Profit Crash That Masked AI Transformation

TCS’s Q3 FY26 results released January 12, 2026 delivered a headline narrative of profit decline that dominated market reaction — but the underlying business transformation toward AI-led services tells a materially different story.

| Financial Metric | Q3 FY26 | Q3 FY25 | YoY Change | Q2 FY26 | QoQ Change |

|---|---|---|---|---|---|

| Revenue from Operations | ₹67,087 Cr | ₹63,973 Cr | +4.87% | ₹65,799 Cr | +2.0% |

| Net Profit | ₹10,657 Cr | ₹12,380 Cr | -13.91% | ₹12,075 Cr | -11.74% |

| Operating Profit Margin | 25.2% | 24.5% | +70 bps | 25.2% | Flat |

| Net Margin | 20.0% | — | — | — | — |

| USD Revenue | $7,509 M | $7,540 M | -0.4% | $7,466 M | +0.6% |

| Constant Currency Growth | — | — | -2.6% YoY | — | +0.8% QoQ |

| Total Contract Value (TCV) | $9.3 B | — | — | $10.0 B | -7% QoQ |

| AI Services Revenue (Annualized) | $1.8 B | — | — | — | +17.3% QoQ (CC) |

| AI as % of Total Revenue | 5.8% | — | — | — | Growing |

| Headcount | 5,82,163 | 6,07,354 | -25,191 (-4.1%) | 5,93,314 | -11,151 |

| Attrition Rate (LTM) | 13.5% | 13.0% | +50 bps | — | — |

Note: Data from TCS Q3 FY26 results presentation, INDmoney, INV, ScanX, The Quint.

The Alarming:

- Net Profit Crashed 14% YoY: ₹10,657 crore versus ₹12,380 crore a year ago — TCS’s worst profit performance in years, driven by:

- Restructuring expenses related to 12,000-employee reduction plan

- One-time impact from new labour code implementation

- Higher SG&A expenses rising to 15.6% of revenue from 14.3%

- Headcount Reduction Accelerating: 11,151 employees cut in Q3 alone, bringing total FY26 YTD reduction to 25,191 (-4.1%) — signaling management’s view that demand weakness requires structural cost cutting, not just hiring freeze

- TCV (Total Contract Value) Falling: $9.3 billion in Q3 down from $10 billion in Q2 — sequential decline in deal wins suggests client spending caution intensifying despite management’s optimistic commentary

- Constant Currency Revenue Declined: -2.6% YoY in constant currency terms reveals underlying weakness masked by favorable Rupee depreciation impact

The Encouraging:

- AI Revenue Hitting $1.8 Billion Annualized: Growing 17.3% QoQ in constant currency, now representing 5.8% of total revenue — on track to become $2+ billion run-rate by Q4 FY26, validating years of AI infrastructure investment

- Operating Margins Expanding Despite Restructuring: 25.2% up from 24.5% YoY demonstrates operational leverage and pricing discipline even as demand softens

- Revenue Growth Positive in Rupee Terms: 4.87% YoY growth is respectable in current environment where Infosys, Wipro, Tech Mahindra all struggling

- OpenAI Partnership Announced: TCS Hypervault data center secured OpenAI as first anchor customer — $1 billion+ strategic relationship potentially generating recurring AI infrastructure revenue for decades

Why Did TCS Stock Crash 31%? The FII Selling Tsunami

TCS’s brutal 31% correction from ₹3,925 to ₹2,686 is not company-specific — it reflects systematic foreign institutional investor (FII) liquidation of Indian IT stocks at scale never seen before.

The FII Exodus from Indian IT:

According to market data, FII outflows from Indian equities exceeded ₹13,000 crore in February 2026 alone, with IT stocks bearing the brunt:

- Infosys: Down 16.5% from peak

- TCS: Down 14-14.8% from peak (some periods)

- HCL Tech: Down 14.2% from peak

The selling is driven by three macro forces:

1. US Client Spending Caution: Major US banking and financial services clients (40%+ of TCS revenue) are reducing discretionary IT spending as:

- Federal Reserve keeps rates higher for longer

- Regional bank stress continues

- Consumer loan demand softening

2. AI Disruption Fear: Investors worry that generative AI tools (ChatGPT, Claude, Copilot) will automate away 30-40% of traditional IT services work — reducing demand for offshore coding, testing, maintenance that built TCS’s $27.9 billion revenue base

3. China+1 Execution Risk: While China+1 manufacturing relocation should benefit Indian IT services, execution has been slower than expected with delays in client decision-making and project go-lives

Why TCS Fell More Than Infosys:

Despite superior Q3 operating margins (TCS 25.2% vs Infosys ~22%), TCS stock underperformed because:

- Higher valuation entering correction (TCS traded 24-25x P/E vs Infosys 20-22x)

- Larger exposure to BFSI sector weakness

- Headcount reduction signaling structural demand concerns, not just efficiency

- Market cap size makes it easier FII liquidation target

The Bull Case: Why Morgan Stanley Says TCS Reaches ₹3,540 (+32% Upside)

Despite the carnage, Morgan Stanley maintained its Overweight rating on TCS with ₹3,540 target price — implying 32% upside from current ₹2,686. The bull thesis rests on TCS successfully transitioning from legacy IT services to AI-led digital transformation partner.

1. AI Revenue Could Hit $4-5 Billion by FY28

At current $1.8 billion annualized growing 17% QoQ, AI services are on track to reach:

- Q4 FY26: $2.1 billion

- FY27: $3.5 billion

- FY28: $5.0 billion (assuming 35-40% CAGR)

If AI reaches 15-20% of total revenue (from current 5.8%) and commands 35-40% margins (vs. 25% blended), AI alone could add ₹5,000-7,000 crore to annual PAT by FY28 — justifying ₹1 lakh crore+ market cap increase.

2. OpenAI Partnership is Strategic, Not Tactical

The Hypervault data center partnership with OpenAI as anchor tenant represents:

- Long-term contracted revenue: Data center leases span 10-15 years with minimum commitments

- GPU infrastructure at scale: 100 MW initial capacity scaling to 1 GW positions TCS as India’s AI infrastructure backbone

- Enterprise ChatGPT access: Exclusive integration across Tata Group companies (Tata Steel, Tata Motors, TCS clients) creates network effects

If Hypervault generates $500 million-1 billion annually in high-margin infrastructure revenue by FY28-FY29, that alone justifies ₹15,000-20,000 crore market cap addition.

3. Valuation at 20x P/E is Reasonable for 12-15% Earnings CAGR

TCS at ₹2,686 trades at 20-21x P/E — actually reasonable for:

- Market-leading operating margins (25.2% vs. peer average 22-23%)

- Superior ROE of 51% (exceptional capital efficiency)

- Debt-free balance sheet with ₹50,000+ crore net cash

- Consistent 12-15% earnings CAGR over 10+ years

If TCS sustains 13-15% revenue growth and expands margins 50-75 bps annually through AI-led services mix improvement, 18-20% earnings growth is achievable — justifying 24-26x forward P/E, implying ₹3,200-3,400 fair value.

4. Market Has Overreacted to Restructuring Costs

The 14% profit decline was largely one-time:

- Restructuring charges related to 12,000 layoffs

- Labour code implementation costs

- Higher SG&A from AI infrastructure buildout

Normalize for these, and core operating profit grew 8-10% YoY — respectable in current weak demand environment. Q4 FY26 and FY27 will show cleaner earnings growth as restructuring concludes.

5. Dividend Yield of 4.7% Provides Downside Protection

TCS announced ₹57 total dividend per share (₹11 interim + ₹46 special) for Q3 FY26 — translating to 4.7% yield at current price. That cash return is attractive versus 6.75% FD rates (considering tax efficiency and growth potential), creating a valuation floor near ₹2,500-2,600 where yield investors step in.

The Bear Case: Why TCS at ₹2,686 Could Fall Another 20% to ₹2,150

The pessimistic scenario argues that TCS’s 31% correction has merely priced in the obvious near-term headwinds, but not the structural risk that AI destroys more traditional IT services revenue than it creates new revenue.

1. AI May Cannibalize More Revenue Than It Creates

While AI services grow 17% QoQ, the hidden story is traditional services declining:

- Application maintenance revenue (30% of total) faces 20-30% productivity gains from Copilot/ChatGPT tools

- Manual testing work (15% of total) being automated by AI agents

- Legacy modernization projects delayed as clients adopt cloud-native AI stacks directly

If traditional services decline 5-8% annually while AI grows to only 15% of revenue, net revenue growth turns negative — destroying the bull thesis entirely.

2. Client Spending Won’t Recover Until Late FY27

BFSI client budgets for FY27 are being finalized now (Feb-Mar 2026) and early indications show:

- Flat to -3% IT budgets for large US banks

- Project deferrals in retail and insurance verticals

- Shift from outsourced offshore work to internal AI tools

TCS management guidance of “discretionary revival in some verticals” is cautiously optimistic — but consensus now models only 6-8% constant currency growth for FY27, down from previous 10-12%. If FY27 growth comes in at 4-5%, earnings disappoint and stock retests ₹2,400-2,500.

3. Margin Expansion is Priced In — No Upside Surprise Likely

Operating margin at 25.2% is already at high end of TCS’s sustainable range (24.5-26%). Further expansion requires:

- Wage inflation staying below 4-5% (unlikely as attrition rises to 13.5%)

- Utilization improving from current 85% (difficult with headcount cuts)

- Offshore mix increasing (clients pushing back, demanding more onsite)

Consensus models 25.5-26% margins for FY27 — just 30-80 bps upside from current 25.2%. That’s not enough to offset revenue growth shortfall risk.

4. FII Selling May Not Be Over

February FII outflows of ₹13,000 crore represent just 3-4 weeks of selling. If global tech selloff intensifies (Nasdaq correction, recession fears), FII could liquidate another $2-3 billion from Indian IT stocks over Q1 FY27.

With TCS commanding ₹9.8 lakh crore market cap, sustained selling pressure could drive stock toward ₹2,400-2,500 levels (18x P/E) before bargain hunters emerge.

5. OpenAI Partnership Could Fail to Scale

While strategically exciting, Hypervault data center faces execution risks:

- 1 GW scale-up requires ₹25,000-35,000 crore capex over 5 years

- GPU availability constrained globally — Nvidia supply may not materialize

- Power grid infrastructure in India may not support 1 GW AI data center demand

- Competitive threat from AWS, Azure, Google Cloud offering enterprise AI at lower cost

If Hypervault generates only $200-300 million revenue versus bull case $1 billion, the partnership adds minimal value to ₹10 lakh crore market cap company.

Key Takeaways

→ TCS at ₹2,686 trades 31% below ₹3,925 52-week high after FII selling tsunami and Q3 net profit crash -14% to ₹10,657 Cr driven by restructuring costs, labour code impact, and 11,151 headcount reduction in single quarter.

→ AI services revenue hit $1.8 billion annualized (+17.3% QoQ constant currency), now 5.8% of total revenue — validates transformation thesis but raises question whether AI creates more revenue than it cannibalizes from traditional services.

→ OpenAI partnership for Hypervault data center (100 MW initial, scaling to 1 GW) is strategically significant — could generate $500M-1B annual high-margin infrastructure revenue if executed, but faces ₹25,000-35,000 Cr capex requirement and GPU availability constraints.

→ Morgan Stanley maintains Overweight with ₹3,540 target (+32% upside) — based on AI reaching $4-5B by FY28 and margins expanding 50-75 bps annually, implying 18-20% earnings CAGR justifying 24-26x forward P/E.

→ FII outflows ₹13,000 Cr in February 2026 hammered IT sector — Infosys -16.5%, TCS -14%, HCL -14.2% from peaks — driven by US client spending caution, AI disruption fears, and China+1 execution delays creating systematic sector de-rating.

→ Valuation at 20-21x P/E appears reasonable for 12-15% earnings CAGR — but bear case argues traditional services cannibalization, client budget cuts persisting into FY27, and margin expansion ceiling at 26% means earnings growth could disappoint, driving retest of ₹2,400-2,500.

→ Dividend yield of 4.7% (₹57 per share including ₹46 special dividend) provides downside cushion — creating valuation floor near ₹2,500-2,600 where income-focused investors step in to capture 5%+ cash returns.

This article is for educational purposes only and does not constitute investment advice. All investment decisions should be made based on individual financial goals, risk tolerance, and in consultation with a SEBI-registered investment advisor.

Data sourced from publicly available information as of February 19-24, 2026. Sources include: NSE India, BSE India, Tickertape, Yahoo Finance, 5paisa, INDmoney, Dhan, Kotak Neo, Groww, Business Standard, TCS Q3 FY26 results presentation, The Quint, INV, ScanX, Morgan Stanley Research, various analyst reports.