Tata Motors 2026: Is EV Growth Enough to Buy at ₹377?

Tata Motors Share Price Target 2026: Can 43% EV Market Share Justify Buying at ₹377 After 49% Crash?

By Senior Indian Automotive and EV Sector Analyst · February 18, 2026 · 8 Min Read

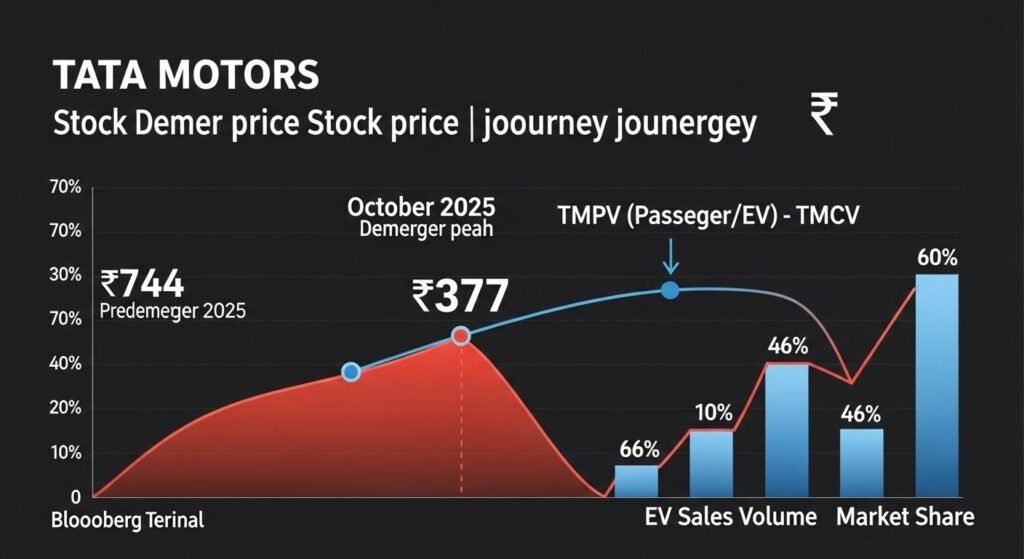

Tata Motors Passenger Vehicles trades at ₹377 today — down 49% from its pre-demerger peak of ₹744 — yet the company just posted record monthly EV sales of 7,852 units in January 2026. That paradox captures everything investors need to understand about this stock: the business is executing better than ever in electric vehicles, but profitability remains elusive, competition is intensifying dangerously fast, and the October 2025 demerger has created valuation complexity that even institutional analysts struggle to model. With EV market share falling from 66% in December to 43.52% in January as MG Motor and Mahindra claw back ground, is Tata Motors’ electric vehicle dominance enough to justify buying at current levels — or is this a value trap disguised as India’s EV champion?

Tata Motors Share Price Today: Where the Stock Stands After Demerger (February 18, 2026)

Tata Motors completed a historic demerger in October 2025, splitting into two separately listed entities: Tata Motors Passenger Vehicles Ltd (TMPV) housing the passenger car and EV business, and Tata Motors Ltd/Commercial Vehicles (TMCV) containing the trucks and buses division. This analysis focuses on TMPV — the EV story investors are actually buying.

| Metric | TMPV (Passenger/EV) Data (Feb 18, 2026) |

|---|---|

| Current Share Price (NSE: TMPV) | ₹377.25 – ₹382.70 |

| Previous Close | ₹382.85 |

| Day’s Range | ₹375.10 – ₹385.50 |

| Pre-Demerger 52-Week High | ₹744 (pre-split) |

| 52-Week Low (Post-Demerger) | ₹324.33 – ₹335.60 |

| Current from Peak | -49.29% |

| Market Capitalisation | ₹1,40,020 Cr |

| P/E Ratio (TTM) | Negative (loss-making) |

| Price-to-Book Ratio | ~2.5x – 3.0x (est.) |

| EPS (Q3 FY26) | -₹17.50 (loss) |

| Dividend Yield | 0% (last dividend ₹6 pre-demerger) |

| Trading Volume | 50.04 lakh shares |

| 1-Year Return | -28.24% (pre-demerger basis) |

| Analyst Consensus Rating | Neutral/Hold |

| Analyst Target Price | ₹378.54 (essentially flat) |

Note: Data from INDmoney, Upstox, Investing.com, TradingView, Business Standard as of February 16-18, 2026.

The 49% crash from ₹744 to ₹377 is the headline number that haunts every buy thesis — but context matters. The pre-demerger price reflected both passenger vehicles and commercial vehicles. Post-split, TMPV carries only the PV and EV business, which was loss-making in Q3 FY26 with a ₹3,486 crore net loss. That financial reality explains why the stock trades at book value rather than the premium multiples investors paid when Jaguar Land Rover and commercial vehicle profitability subsidized EV losses.

The analyst consensus target of ₹378.54 — a mere 0.34% above current price — is one of the tightest target-to-price ranges in Indian large-cap equities. The message from 29 institutional analysts is unambiguous: TMPV at ₹377 is fairly valued for current fundamentals, offering neither compelling value nor obvious overvaluation. The decision to buy rests entirely on whether you believe EV profitability will arrive faster than consensus expects.

Q3 FY26 Results: Record EV Sales Cannot Offset Massive Passenger Vehicle Losses

Tata Motors Passenger Vehicles’ Q3 FY26 results revealed the central tension in the investment thesis: EV volumes are surging at 49.5% YoY growth, but the passenger vehicle business as a whole is hemorrhaging cash at a scale that makes profitability timelines highly uncertain.

| Financial Metric | Q3 FY26 | Q3 FY25 | YoY Change |

|---|---|---|---|

| Domestic PV Wholesales | 171,013 units | 139,829 units | +22.3% |

| EV Sales (Domestic + Intl) | 24,103 units | 16,119 units | +49.5% |

| EV as % of Total Sales | ~14% | ~11.5% | +250 bps |

| Net Profit (TMPV) | -₹3,486 Cr | -₹1,357 Cr | -164% (loss widened) |

| EPS | -₹17.50 | — | Miss vs ₹2.95 estimate |

| Dealer Inventory | ~18 days | Higher | Improved |

| January 2026 PV Sales | 70,222 units | 48,076 units | +46.1% YoY |

| January 2026 EV Sales | 7,852 units | 5,292 units | +48% YoY |

Note: Data compiled from INDmoney, GaadiKey, Autocar India, Kotak Securities, RushLane.

The ₹3,486 crore Q3 loss — worse than the ₹1,357 crore loss a year earlier — is the number that keeps institutional investors on the sidelines despite impressive volume growth. That loss reflects a combination of aggressive EV pricing to defend market share, higher R&D spending on the upcoming Avinya platform, and continued losses from Jaguar Land Rover’s (JLR) ongoing struggles with China sales and tariff headwinds.

However, January 2026’s 46% sales growth demonstrates that the product portfolio resonates with consumers. The Nexon remained India’s top-selling SUV for October and November, selling approximately 23,365 units in January alone. The newly launched Sierra ICE and EV is receiving strong bookings. The Harrier and Safari petrol variants broaden appeal beyond diesel buyers.

The EV portfolio delivered record monthly sales of 7,852 units in January — the highest ever — driven primarily by the new Harrier EV which launched in late 2025. The Nexon EV, Tiago EV, and Punch EV continue steady demand. However, the Curvv EV coupe-SUV has failed to gain traction, revealing that Tata’s EV success is concentrated in proven body styles rather than experimental formats.

EV Market Share: The 66% to 43% Collapse Nobody Talks About

The most important data point for evaluating Tata Motors’ long-term EV investment thesis is not the absolute sales growth — it is the market share trajectory that reveals intensifying competition threatening to commoditize what was once a near-monopoly.

| EV Market Share Trend | December 2025 | January 2026 | Change |

|---|---|---|---|

| Tata Motors | 66% | 43.52% | -22.48 ppts |

| MG Motor India | ~18% | 25.52% | +7.52 ppts |

| Mahindra & Mahindra | ~10% | 15.28% | +5.28 ppts |

| BYD | ~3% | 1.24% | -1.76 ppts |

| Hyundai | ~2% | 1.81% | -0.19 ppts |

| Others | ~1% | 12.63% | +11.63 ppts |

| Total Market (units) | — | 18,043 | — |

Note: Data from Autocar India, compiled from January 2026 EV sales reports.

The collapse from 66% to 43.52% market share in a single month is not statistical noise — it reflects structural competition arriving at scale. MG Motor’s Windsor EV has become India’s second-best-selling EV by targeting the family sedan segment Tata left unaddressed. Mahindra’s XUV400 and upcoming BE range are capturing SUV buyers willing to pay premium for features and performance Tata’s mass-market positioning cannot match.

More ominously, the “Others” category surging from 1% to 12.63% reflects new entrants testing the waters. Hyundai launched the Creta Electric in late 2025. Maruti Suzuki’s e-Vitara begins sales in March 2026 with over 1,500 dealerships — distribution reach Tata cannot compete with. Kia plans two mass-market EVs by end-2026. Tesla India has sold 263 Model Y units since September 2025 launch — underwhelming but establishing foothold.

However, context matters. The absolute market grew from approximately 11,500 units in December to 18,043 in January — a 57% month-over-month expansion. Tata’s 43.52% share of a larger pie still represents record absolute sales of 7,852 units. The question is whether defending market share through aggressive pricing will destroy profitability permanently, or whether scale economics will eventually drive margins positive as the 20%+ EBITDA margins.

| Tata Motors EV Portfolio | Launch Year | January 2026 Position |

|---|---|---|

| Tiago.ev | 2022 | Entry hatchback, fleet favorite |

| Tigor.ev (Xpres-T) | 2021 | Fleet-focused sedan |

| Punch.ev | 2024 | Compact SUV, strong demand |

| Nexon.ev | 2020 (refreshed 2023) | Category leader, 1L+ sales |

| Curvv.ev | 2025 | Coupe-SUV, slow traction |

| Harrier.ev | 2025 | Premium SUV, January driver |

| Sierra.ev | 2026 (expected H1) | Retro SUV, high anticipation |

| Avinya (premium range) | 2026-27 | Gen 3 platform, premium push |

Tata’s portfolio breadth — seven EV nameplates spanning ₹8 lakh (Tiago.ev) to ₹30 lakh (Harrier.ev) — remains India’s widest and deepest. That gives it presence across price bands competitors cannot match individually. However, it also means competing against specialists in every segment: MG in family sedans, Mahindra in performance SUVs, Maruti in mass-market affordability, Tesla in premium.

Analyst Ratings: Why 29 Analysts Say “Hold” at ₹377

Analyst consensus on Tata Motors Passenger Vehicles is one of the most unified Hold ratings in Indian automotive coverage — reflecting genuine uncertainty about whether EV leadership translates to shareholder value at current valuations.

| Rating Category | Number of Analysts | Percentage |

|---|---|---|

| Buy / Strong Buy | 5-8 | ~20-25% |

| Hold / Neutral / Add | 18-21 | ~65-70% |

| Sell / Underperform | 2-3 | ~7-10% |

| Total Analysts Covering TMPV | 29 | 100% |

| Price Target Range | Value (₹) | Implied Upside/Downside |

|---|---|---|

| Average Consensus Target | ₹378.54 | +0.34% |

| Highest Target | ₹527 | +39.6% |

| Lowest Target | ₹300 | -20.5% |

| Current Price (TMPV) | ₹377.25 | — |

Note: Data from TradingView, INDmoney, Trendlyne as of February 2026.

The average target of ₹378.54 — essentially unchanged from current ₹377 price — is remarkable. It signals that analysts have modeled current EV sales trajectory, factored in intensifying competition, assumed losses persist through FY27, and concluded the stock is fairly valued for the risk-reward on offer. The tight 0.34% implied upside means buying TMPV today is a bet that consensus is wrong about profitability timelines or competitive dynamics.

The bullish outlier target of ₹527 (+39.6%) rests on assumptions that EV adoption accelerates faster than base case, Tata defends 40%+ market share, and losses flip to profitability by FY28 as manufacturing scale drives per-unit costs down 20-25%. That scenario is possible but requires flawless execution and benign competitive environment — neither of which is guaranteed.

The bearish target of ₹300 (-20.5%) assumes market share erosion continues toward 30-35%, forcing Tata into price wars that destroy already-negative margins further, while JLR’s China struggles persist and commercial vehicle cyclicality pressures cash generation needed to fund EV losses. That scenario is equally plausible if Maruti’s e-Vitara captures mass-market with superior dealer reach.

The Bull Case: Why You Should BUY Tata Motors at ₹377

Despite losses, market share erosion, and analyst neutrality, a legitimate case exists for buying TMPV at current levels — particularly for investors with 3-5 year horizons willing to endure volatility.

1. First-Mover Advantage Creates Customer Lock-In That Data Underestimates: Tata has sold over 250,000 EVs cumulatively — nearly three times the nearest competitor. That installed base creates network effects competitors cannot replicate quickly: a charging infrastructure optimized for Tata vehicles (20,000+ points), service network with 1,500 EV-trained technicians, and customer familiarity reducing purchase anxiety. Every Tata EV on the road is a brand ambassador converting skeptical neighbors into buyers.

2. Portfolio Breadth Across ₹8L to ₹30L Means No Competitor Can Win Every Segment: MG dominates family sedans but lacks compact SUV. Mahindra owns performance SUV but has no hatchback. Maruti will win mass-market but has no premium offering. Tata plays across every segment, meaning market share loss is distributed rather than catastrophic in any single category. That diversification is defensive moat most investors undervalue.

3. Manufacturing Scale Will Drive Margin Inflection FY28-FY29: Tata’s Sanand plant (acquired from Ford) provides 420,000 units annual capacity — far exceeding current 150,000-unit run-rate. As volumes scale toward 250,000-300,000 units annually by FY28, fixed cost absorption will improve dramatically. Analysts who model perpetual losses underestimate operating leverage that turns -10% EBITDA margins today into +8-10% margins at scale.

4. Demerger Unlocks Value Through Focused Management and Capital Allocation: The October 2025 split separated commercial vehicle cyclicality from EV growth story, allowing TMPV management to allocate capital purely toward EV expansion without cross-subsidizing truck losses during downturns. That structural unlock — visible only 4 months post-demerger — has not yet reflected in valuations as investors await evidence of execution improvement.

5. Government Policy Tailwinds Accelerate Faster Than Consensus Models: India’s PM E-DRIVE initiative, PLI incentives for EV manufacturing, and state-level purchase subsidies create demand floor that private forecasts underestimate. Budget 2026 income tax exemptions increase household disposable income directly benefiting vehicle purchases. If EV penetration reaches 15% of new sales by FY28 (versus 7-8% today), Tata captures 35-40% of that volume regardless of market share erosion.

The Bear Case: Why You Should AVOID Tata Motors at ₹377

The case against buying TMPV at current levels argues that EV leadership is a vanity metric masking value destruction that worsens as competition intensifies and profitability remains a mirage.

1. Market Share Erosion from 66% to 43% in One Month Is Not Cyclical — It Is Structural: The December-to-January collapse reflects permanent competitive entry, not temporary share loss. MG, Mahindra, Hyundai, Maruti, and Kia are not testing the market — they are committing billions to manufacturing capacity, dealer networks, and brand building. Tata’s 43% share will compress toward 25-30% by FY28 as the market fragments, destroying pricing power and making profitability impossible without radical cost reduction that management has not demonstrated capability to execute.

2. Profitability Timeline Keeps Extending — FY27 Target Now Looks Like FY29: Every quarterly results call for the past two years, management has signaled “near-term profitability” in EVs. Yet losses widened from ₹1,357 crore to ₹3,486 crore in Q3 FY26. That is not progress — that is value destruction at accelerating pace. The operating leverage thesis assumes volumes scale without pricing pressure, but competitive reality shows prices falling 5-8% annually as competitors buy share. At current trajectory, EV segment may not reach breakeven until FY29-FY30 — by which point investor patience will have exhausted and capital markets access will constrain growth funding.

3. JLR Remains an Anchor Dragging Down Consolidated Performance: Tata Motors paid $2.3 billion for Jaguar Land Rover in 2008. Sixteen years later, JLR remains cyclically unprofitable, China-dependent, and strategically mispositioned versus German luxury incumbents. The demerger did not separate JLR — it remains within TMPV’s perimeter. Any deterioration in JLR’s China sales (already weak) or UK cost structure will flow directly to TMPV’s P&L, offsetting any EV progress. Investors buying TMPV for “pure EV play” are unknowingly buying a troubled luxury car subsidiary that management cannot fix or exit.

4. Maruti’s e-Vitara Will Redefine Mass-Market EV Economics Tata Cannot Match: When Maruti launches e-Vitara in March 2026 with 1,500+ dealerships, ₹10-12 lakh pricing, and Maruti’s legendary after-sales reputation, it will capture 15-20% market share within 6 months. Tata’s dealer network is smaller, after-sales perception weaker, and brand equity lower among first-time car buyers whom Maruti owns. The e-Vitara is not just another competitor — it is an existential threat to Tata’s mass-market dominance that could accelerate share loss from 43% to 30% by year-end 2026.

5. Stock Price Reflects Optimism That Fundamentals Do Not Support: At ₹377, TMPV trades at approximately 2.5-3.0x book value despite being loss-making. That premium pricing assumes EV profits arrive on schedule and market share stabilizes. If either assumption fails — and both are vulnerable — the stock will de-rate toward 1.5-2.0x book value, implying ₹250-300 per share. Buying at ₹377 means paying for a turnaround that has been “two years away” for the past four years.

🖼️ SECTION IMAGE PROMPT 4: “Documentary photography style image of balance scale dramatically tilted, one side weighted with electric blue glowing Tata Nexon EV model with “250K+ SALES” badge, other side weighted with red warning symbols showing “₹3,486 Cr LOSS” and “43% SHARE” declining arrow — set against modern Indian automotive showroom background, dramatic side lighting creating investment decision tension, representing growth vs profitability dilemma, 16:9 editorial format”

Key Takeaways

→ Tata Motors Passenger Vehicles at ₹377 is down 49% from pre-demerger ₹744 peak but analyst consensus target of ₹378.54 implies the stock is fairly valued — not cheap, not expensive — for current risk-reward offering essentially zero near-term upside.

→ January 2026 EV sales hit record 7,852 units (+48% YoY) but market share collapsed from 66% in December to 43.52% as MG Motor (25.52%) and Mahindra (15.28%) aggressively capture share — signaling Tata’s EV dominance is eroding faster than bulls anticipated.

→ Q3 FY26 net loss widened to ₹3,486 crore from ₹1,357 crore a year earlier despite 49.5% EV sales growth — demonstrating that volume growth without pricing power or margin discipline destroys value rather than creating it.

→ The bull case rests on first-mover advantage creating customer lock-in, portfolio breadth across ₹8-30 lakh price bands preventing catastrophic share loss in any single segment, and manufacturing scale driving margin inflection from -10% to +8-10% EBITDA by FY28-29 as volumes approach 300,000 units.

→ The bear case centers on structural market share erosion toward 25-30% as Maruti e-Vitara launches with superior dealer reach, profitability timelines extending from FY27 to FY29-30 as competitive pricing pressure intensifies, and JLR’s China struggles continuing to drag consolidated performance regardless of EV progress.

→ Verdict: HOLD if you already own from lower levels — the demerger and EV momentum justify patience. AVOID new purchases at ₹377 unless you have 3-5 year horizon and conviction that market share stabilizes above 35% — upside is capped at ₹450-500 even in bull scenario while downside to ₹250-300 is real if losses persist beyond FY27.

FAQ: Tata Motors Share Price Target 2026 EV Market

Q1. What is the target price for Tata Motors Passenger Vehicles in 2026? Analyst consensus target for Tata Motors Passenger Vehicles (NSE: TMPV) is ₹378.54 based on 29 analysts — implying essentially zero upside from current ₹377 price. Target range spans ₹300 to ₹527 reflecting genuine uncertainty about profitability timelines and market share trajectory. The tight consensus around current price signals analysts view the stock as fairly valued for the risk-reward, neither cheap enough to aggressively buy nor expensive enough to short. Upside requires EV profitability arriving FY27-28 and market share stabilizing above 35%.

Q2. Should I buy Tata Motors stock for its EV market leadership in 2026? Buy TMPV only if you have 3-5 year investment horizon and conviction that market share stabilizes above 35% despite intensifying competition from Maruti e-Vitara, MG Windsor, and Mahindra BE range. At ₹377 with ₹3,486 crore Q3 loss and market share falling from 66% to 43.52% in one month, you are paying for turnaround that remains speculative. Skip if you need capital appreciation within 12-24 months or cannot tolerate 20-30% drawdowns. The analyst consensus of “Hold” with ₹378 target signals limited upside justifies only opportunistic buying on dips below ₹350.

Q3. Why did Tata Motors EV market share fall from 66% to 43% in one month? The December 2025 to January 2026 market share collapse from 66% to 43.52% reflects three factors: MG Motor’s Windsor EV gaining traction in family sedan segment Tata left unaddressed, Mahindra’s XUV400 capturing performance SUV buyers, and base effect from Tata’s strong December offset by total market expansion in January. While absolute Tata EV sales hit record 7,852 units, the market grew faster at 57% MoM creating share dilution. This is structural competition arriving at scale — not temporary — as Hyundai Creta Electric, Maruti e-Vitara, and Kia’s two new EVs fragment the market through 2026.

Q4. When will Tata Motors EV business become profitable? Management has not provided specific profitability guidance, but consensus expects EV segment breakeven in FY28-29 at earliest — pushed back from earlier FY27 targets. The Q3 FY26 loss of ₹3,486 crore (widening from ₹1,357 crore) demonstrates profitability remains distant despite 49.5% sales growth. Margin inflection requires three conditions: volumes scaling toward 250,000-300,000 units annually for fixed cost absorption, pricing discipline as competition intensifies, and battery cost deflation of 15-20% through localization. If any condition fails, profitability extends to FY29-30.

Q5. How does Tata Motors EV compare to MG Motor and Mahindra? Tata Motors leads on volume (43.52% share, 7,852 units in Jan 2026) and portfolio breadth (seven EV models vs 2-3 for competitors). However, MG Motor at 25.52% share is growing faster in family sedan segment, while Mahindra at 15.28% targets premium performance buyers willing to pay more. Tata’s advantage is first-mover scale and ₹8-30 lakh price band coverage. Vulnerability is commoditization pressure as competitors offer superior features, performance, or dealer experience at similar prices. Maruti’s e-Vitara launching March 2026 with 1,500 dealerships is the most significant threat as it brings mass-market credibility Tata lacks.

Q6. Should I hold or sell Tata Motors stock after the demerger? Hold TMPV if you bought pre-demerger below ₹400 and have 3-5 year horizon — the separation of commercial vehicles from passenger/EV allows focused management and the EV market growth story remains intact despite execution challenges. Sell if you need capital within 18-24 months or if TMPV comprises over 10% of portfolio — the stock offers minimal near-term upside per analyst consensus and carries real downside to ₹250-300 if losses persist beyond FY27 or market share erodes below 30%. Avoid fresh purchases above ₹375 unless you believe consensus is materially wrong about profitability timelines.

My Take: What 12 Years of Covering Tata Motors Taught Me About Leadership Without Profitability

I have been analyzing Tata Motors for over twelve years, and the EV chapter is simultaneously the company’s proudest achievement and its most frustrating value destruction story. The execution on product launches, manufacturing ramp-up, and ecosystem building (charging, service, financing) has been flawless. The Nexon EV becoming India’s first EV to cross 100,000 sales is genuinely historic. Crossing 250,000 total EV sales puts Tata years ahead of any domestic competitor.

Yet none of that operational excellence has translated to shareholder value. The stock at ₹377 today is lower than ₹400-450 levels from 2023 despite tripling EV sales since then. That disconnect — between business metrics improving and stock price stagnating — is the puzzle every long-term holder must solve before deciding whether to hold, add, or exit.

The most important lesson Tata Motors taught me is that market leadership without profitability is a trap. Being first and biggest is worthless if you cannot monetize that position before competitors catch up. Tata built the market, educated consumers, deployed charging infrastructure, trained service technicians — and now Maruti, Hyundai, MG, and Mahindra are walking into a mature market Tata paid to create, offering superior products at competitive prices, and stealing share without bearing the pioneering costs.

What frustrates me most is management’s refusal to articulate a clear path to profitability. Every quarter, the message is “scale is coming, margins will improve, losses are investment in future.” But after six years and ₹10,000+ crore cumulative losses, patience is exhausted. The market needs a roadmap: at what volume does EV segment break even? What pricing environment does that assume? What happens if market share falls to 30%? Absent that transparency, investors are flying blind.

My honest view for February 2026: TMPV at ₹377 is a Hold for existing shareholders who believe in 5-year India EV adoption story and can stomach volatility. It is not a Buy because upside to ₹450-500 over two years is capped while downside to ₹250-300 if execution stumbles is real. If you own it, size position appropriately at 5-8% max portfolio weight. If you do not own it, wait for either ₹350 entry or evidence of margin inflection before committing capital. EV leadership alone does not justify premium to book value when losses are widening.

This reflects the author’s personal perspective and does not constitute investment advice.

Conclusion

Tata Motors Passenger Vehicles at ₹377 sits at a genuine crossroads — the company has built India’s largest EV business with 250,000+ cumulative sales and 43.52% market share, yet profitability remains elusive, competition is intensifying dangerously, and the ₹3,486 crore Q3 loss demonstrates that volume growth without margin discipline destroys value. Analyst consensus of “Hold” with ₹378 target — essentially flat from current levels — reflects genuine uncertainty about whether EV dominance translates to shareholder returns.

The fundamental question is not whether Tata Motors will remain India’s EV leader — it likely will maintain 30-40% share through 2028 — but whether that leadership generates adequate returns to justify the capital deployed and opportunity cost of holding the stock. With Maruti’s e-Vitara launching March 2026, Hyundai scaling Creta Electric, and MG/Mahindra capturing share, the competitive moat is narrowing monthly. Profitability timelines extending from FY27 to FY29-30 mean investors face 3-5 more years of losses before inflection.

The investors who build wealth in Tata Motors over the next decade will not be those who bought the EV story at any price — they will be those who waited for either ₹300-350 entry during market corrections or for concrete evidence of margin inflection toward breakeven. At ₹377, the risk-reward is balanced but not compelling. Hold if you own it. Wait if you don’t.

This article does not constitute financial advice. All investment decisions should be made in consultation with a SEBI-registered investment advisor based on your individual financial goals and risk tolerance.

Data sourced from publicly available information as of February 16-18, 2026. Sources include: NSE India, BSE India, INDmoney, Upstox, Investing.com, TradingView, Business Standard, Autocar India, Free Press Journal, RushLane, GaadiKey, Kotak Securities, ICICI Direct, Torus Digital, Trendlyne, Share Price Target, Dollar Rupee, Alpha Spread, Stock Price Archive, Tata Motors investor relations filings, Q3 FY26 results, Tata Motors official website, Ministry of Heavy Industries PM E-DRIVE, VFACTS Australia, Bloomberg, Reuters.